Lending and borrowing on FreeTON

Introduction

DeFi was born as a competitive vehicle for decentralized financial applications that act as various financial incentives: transactions and payment solutions, borrowing, lending, and real asset tokenization. DeFi solves the problems with centralized control, limited access, low efficiency, lack of interconnectivity and transparency now and can do more in the future. In this paper, I’ll try to describe the current status and actors of the DeFi market and propose a vision of the future opportunities that DeFi unlocks for the FreeTON ecosystem.

FreeTON is probably one of the most promising platforms for lending and borrowing development, due to its open-source nature, focus on cooperation within the community and solid expertise not only among the developers but ecosystem members as well.

Thus, in this submission I’ll try to present my vision on how financial instruments, as well as borrower and lenders, can gain the values from FreeTON incentives, what are the risks and opportunities as well as propose several conceptual ideas on how to proceed.

I’m Sergey Kalinin, Head of Product of UAX - a first gasless dual-layer stablecoin with delegated transfer infrastructure, fully developed on FreeTON by Kuna Exchange. Previously I was working in Dfinance, a project of Wings Foundation, dedicated to natural-language programming financial instruments on Cosmos. As well as a management executive in several financial and blockchain companies.

Market conditions

In the first place, it is necessary to accept that despite the fact that DeFi is perceived as a hammer for the traditional financial system, many of the approaches and tools are based on ideas that have already existed for many years in finance. In particular, the topic of this work is lending, and many of the principles of DeFi came from the banking sector. These operations are based on the principles of ABL - asset-based lending, where loans are issued on the basis of asset’ over-collateral.

Although DeFi aspires to create an independent, parallel financial system based on code rather than legal enforcement, the key component of the DeFi system is actually based on traditional financial market infrastructure. The most critical link between the two systems can be found in stablecoins. These include US Dollar-denominated stable tokens circulating on public blockchains, which are in principle backed by commercial banks tied to financial institutions dealing with US Dollars.

Stablecoins are a vital instrument for DeFi transactions because they introduce collateral denominated in fiat while keeping the open transaction environment of the public blockchain. However, the vast majority of stablecoins derive value from the underlying US Dollar instrument and therefore rely on the issuer of the underlying instrument and the financial institution that deposits US dollars. But I have to admit that these “fiat-backed” stablecoins are an important part of the fast and effective expansion of financial instruments, laying on the “proof-of reserve” concept, which is the core feature of UAX - stablecoin on FreeTON blockchain. That’s how we can revert fiat reserves into algorithmic stablecoins.

This principle was developed in UAX whitepaper. In short: fiat-backed stablecoin emission becomes the fuel for using this stablecoin in smart contracts which gain more credibility and solvency due to the fact of real-world collateral.

By the way. Ethereum-based stablecoins backed with fiat and circulate on public blockchains, in April 2021 were worth at least 20 times more of non-redeemable stablecoins issued against crypto-native collateral. Even some of the most decentralized stablecoins, like MakerDAO have introduced points of compromise where dollar-denominated assets like USDC can be used against the crypto collateral within a smart contract.

The top five DeFi protocols by USD-equivalent amount of collateral supplied – MakerDAO, Curve, Uniswap, Aave, and Compound – collectively host $3.818 billion in USDC and $1.06 billion in Tether (USDT) in deposits (April 2021) These figures represent 42% of outstanding USDC and 5.2% of USDT respectively circulating on Ethereum.

Risks

Despite the decentralized nature of the smart contacts and DeFi itself, humans are still in the game. It is impossible for now to eliminate the offline interactions and relations between people and this is the place where risks arise. The DeFi core protocol tends to retain a certain degree of human participation of the controlling entity. This is a means of mitigating risks when they arise, but if the administrator himself is threatened, maliciously or in some way compromised, it can also pose a potential threat to such systems. This paper is not intended to give the answers on how Free TON will deal with such risks and threats, but we have to understand that effective and proven solutions across those topics will gain a lot of attention and market appreciation in the blockchain space.

Miner extractable value (MEV) - is made possible due to the innate transparency of blockchain and the possibility of gaining priority by outbidding other users. With the increase in transaction complexity, there are more opportunities for risk-free arbitrage and unfair execution, like front-running.

Oracles - the vulnerability category is related to the problem caused by the blockchain data provider. In DeFi, the oracle provides external information to the smart contract execution. For example, a lending agreement that uses tokens as collateral should know the value of the given tokens (in standard terms such as US Dollars) and use smart contracts that use market information provided by oracle and its data feed. Some DeFi protocols are based on oracles, and price input is essential for triggering liquidation, deleveraging, margin calls, and other forms of automatic collateral management. Therefore, for these protocols, the oracle failure in any form can be catastrophic.

Admin keys - there are many risks associated with keys management in most active and high-profile DeFi projects. Like the keys loss, the theft of deposits by insiders, theft through extortion or third-party hack, and regulatory pressure. It means that the assets held in the contract with the administrator key as the intermediary should be understood as custody, rather than a fully sovereign interaction between the users and blockchain. Adding more signers to the multi-signature key setup just means that user deposits are kept by a consortium of insiders, rather than by a single entity.

Law enforcement - in many cases, DeFi entities are financed by issuing pseudo-capital (or equity) tokens, which represent claims for certain cash flows generated by the protocol. These tokens have proven to be an important financing tool for the DeFi protocols’ development. Many of these tokens grant token holders some basic governance rights, as well as implicit or direct claims to the cash flows generated through the lending protocols. These pseudo-equity tokens supporting DeFi are not registered as securities but are circulated in a decentralized financial infrastructure. If such pseudo-equity tokens are identified as unregistered securities by securities regulators, the financing and governance models of these DeFi projects will be significantly affected. In addition, many DeFi agreements subsidize liquidity by issuing new units (known as LP-token) to end-users. If these tokens are removed from the listing, their liquidity and value will suffer, and the utility of these protocols will be reduced.

We know that blockchain technologies bring many benefits so far. But the tools or processes used to disintermediate or gain efficiency also have costs in recourse, reversibility and risk management.

Solutions

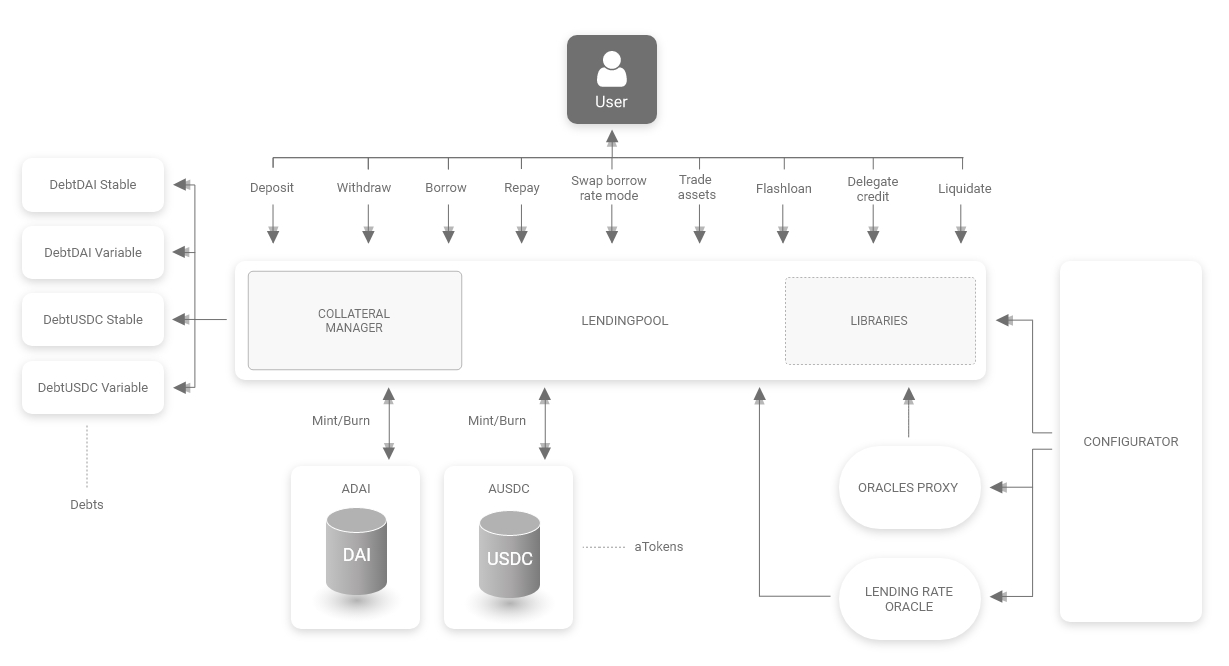

Loans are an essential part of the DeFi ecosystem within FreeTON. Everyone has access to the platform and can potentially borrow money or provide liquidity to earn interest. As such, DeFi loans are completely permissionless and not reliant on trusted relationships.

My assumptions are based on the fact that for a full-fledged operation, convenient and fast interaction with liquidity providers, wide opportunities for liquidations and deleveraging should exist, as well as oracles and price discovery mechanisms are necessary.

I guess that initial steps should be realized in the form of collateralized lending/borrowing where loans can be fully secured with collateral. The collateral is locked in a smart contract and only released once the debt is repaid. Collateralized loan platforms exist in three variations: Collateralized debt positions, pooled collateralized debt markets, and P2P collateralized debt markets. Collateralized debt positions (CDP) are loans that use newly created tokens, while debt markets use existing tokens and require a match between borrowing and a lending party.

In Free TON we can realize all of them, but with a different timeline and pace. Also, I see a proper perspective for a combined approach between the fiat-backed and crypto-collateralized assets, where traditional finance is dealing as the provider of backed liquidity. While this liquidity is the main source for CDP contracts, when existing tokens, secured by liquidity can be lent/borrowed against the crypto.

Let’s try to outline the mechanics which we can apply at FreeTON. The main assumption will be that credit is not only a product that provides access to liquidity and the possibility of income on it, but also is the underlying asset for more advanced credit derivatives that can be freely issued and used within the TON ecosystem. For example, Debt Risk Options (DRO) allow the borrower to sell credit obligations, and the buyer of such obligations is getting the property right to the underlying collateral.

Any market participant can become a part of the Free TON financial system. This can be as through a CDP contract when a new stable coin is issued by DAO in exchange for a pledge in TON Crystal. In the future, other blockchain assets can and should become full-fledged collateral instruments. The second option is the principle of a two-layer stablecoin, which was adopted during creating UAX, where liquidity appears in the system through “proof-of-reserve” and legal entity or market player, based on a legally confirmed scheme of interconnection with the local banking system. This principle can be implemented in other jurisdictions with certain changes.

The legal entity issues the “proof-of-reserve” stablecoin with reserves that are held in the financial institution as collateral. This is the easiest way to put liquidity into the Free TON system. There is a UAX proof-of-concept, where the stablecoins are minted against the fiat-denominated derivatives with normal circulation.

Stablecoin is marketed across the Free TON ecosystem as a mean of exchange and the base layer for various financial applications and borrow/lending mechanisms.

New financial specifications and applications are developing as ready-to-use solutions for the market. It means that independent developers are involved in the process development of credit, lending/borrowing and other financial use-case tools. The community is responsible for providing proper financial tools as the products.

Any eligible person can buy stablecoins from a trusted source of “proof-of-reserve” funds, implement some kinds of smart contracts as SaaS and “open” his own decentralized financial institution like a “private bank”

“Private bank” independently deals with lending/borrowing operations according to the smart-contract logic, sets the level of loan-to-value (LTV), chooses the type of collateral, loan repayment terms and liquidation of collateral, or sells the debt.

The ecosystem should provide trusted infrastructure for borrowing/lending activities - liquidation auctions through the DEX; price discovery through the oracles; bridges and fiat gateways through the commercial protocols and market participants.

“Banks” deal independently, compete with each other for the users. In this situation we have the system where functions are divided as there are liquidity providers who mint the backed stablecoin; market intermediaries which buy the liquidity to provide it for the lending with interest; users who use their crypto-assets as collateral to borrow the stablecoin and use it within the Free TON ecosystem.

There is a secondary debt market where “bank” can sell the credit via DRO, where new market players are in Free TON ecosystem - risk sellers/risk buyers in form of credit derivatives

Future development ideas

I see significant perspectives in negotiable bilateral contracts (a reciprocal arrangement between two parties to perform an action in exchange for the other party’s action) that help the users to manage their exposure to credit risks. The buyer pays a fee (premium) to the seller (who is taking a specific risk in return for the premium).

DROs refer to various instruments and techniques designed to provide the option holder with the right, but not the obligation, to perform some predefined action - such as buy or sell an underlying asset at a preset liquidation price. The next step of development could be a simplified debt risk option, focused on use within the DeFi ecosystem.

Debt Risk Option transfers the credit risk (or the risk of a default event) of a borrower, also known as CDP creator in the Free TON ecosystem. CDP creator (“Risk Seller”) can issue a Debt Risk Option where he wants to sell the risk of the loan taken and get additional revenue if he believes that the risk event will not happen in the future. In exchange, someone on the market may think that a given risk can happen in the future and the loan is not well secured or the premium is low. Therefore he wants to buy this risk (“Risk Buyer’’) of the event and pay a non-refundable premium as the price of the given option, to acquire the underlying leveraged collateral at the liquidation price, and a swap deal with the upfront premium fee occurs.

As a CDP creator (or “borrower”) you can create an option and sell the risk of default on your loan. You can set up the price of this financial instrument on your own. There is no pricing discovery in classical, the Risk Seller estimates the price as effective for his collateral. But if you do not estimate your option and maturity date and price it fairly, no one will buy it. It is a double-sided contract and a fair price is crucial. IMPORTANT - if you sold the debt risk option, you cannot change the CDP or the collateral and its assets.

Whatever loan you take, you have to deposit collateral no less than 150% of the loan, which is a minimal 66% loan-to-value and a margin call at the same level. Note that it is highly recommended to use a lower LTV to avoid instant liquidation.

Now the Risk Seller can sell the token either OTC or using the DEX. If no one wants to buy it, there is no deal and the option token just gets burned at the maturity date. But if someone on the market thinks your loan is on fire, is ready to pay the premium (and thus gets the right to purchase your collateral at a discount in case of default), there is a deal.

If the loan underlying collateral value drops to 150% and a margin call occurs, the Risk Seller has the right but not the obligation to buy back the TONs (or other collateral) with the current price within the emergency zone which is 130% of the loan value. If the loan value drops to 130% collateral and the Risk Buyer does not buy the collateral, then the CDP will be liquidated and the CDP loan amount in UAX will be returned to the liquidity pool and the rest (if any) will be sent to the Borrower (Risk Seller). The Risk Seller retains the option premium and loan because the Risk Buyer already bought the collateral.

But if there is no default event and the Risk Seller pays back the loan thus releases the collateral and gets the option premium. The Risk Buyer had no opportunity for the option to be realized and lost the option premium.

Conclusion

Within Free TON it is possible to build up an integrated system for borrowing/lending against the native TON Crystals as well as via a new type of dual-layer stablecoins, relying on interconnection with traditional finance systems. But, for the given financial activities DEX as a tool for collateral liquidation, deleveraging and auctioning are crucial. As well as trusted oracles is an important part of price discovery and collateral management. Then we can provide financial infrastructure and Free TON scalability as a vital part of the financial environment where almost anyone can be your own financial institution.

I have a much more detailed vision on how to proceed and what are the next steps and would be happy to become a part of the Free TON financial revolution. Also, there is some initial work already done. I would be happy to join as an active member of Free TON DeFi subgove to develop lending and borrowing solutions.

Sergey Kalinin, Telegram: @s_kalinin